Sellers, Be Careful: Overpricing Could Cost You Big in Today’s Market

As a real estate agent, I’ve seen it time and time again—homeowners clinging to pandemic-era price expectations, setting themselves up for frustration in today’s shifting market.

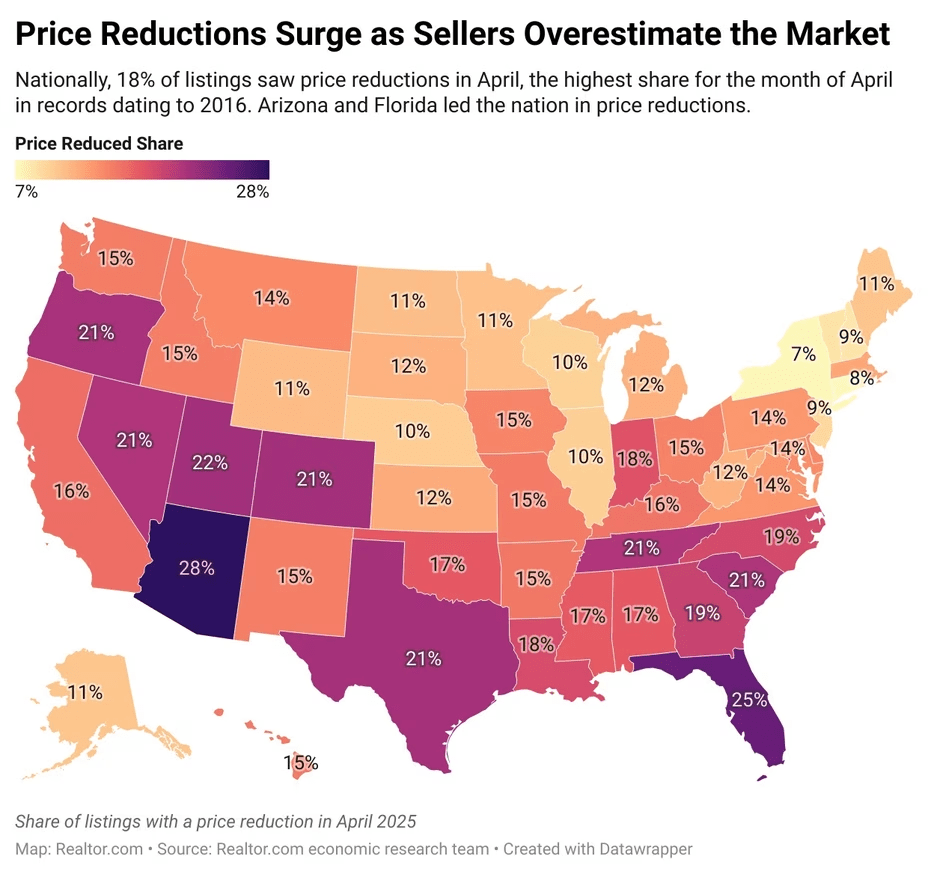

Back in the COVID-19 housing boom, bidding wars and skyrocketing values were the norm. Many sellers who bought during that time are now expecting similar results. But market conditions have changed. Buyer demand has softened, and price cuts are becoming more common. In fact, April saw a record-high share of listings with price reductions nationwide, according to Realtor.com.

Despite this, over 80% of homeowners surveyed still believe they’ll get asking price or more. But homes that are overpriced simply sit—and the longer they sit, the harder they are to sell.

You Still Stand to Win—Just Be Realistic

The good news? Even if you don’t hit your dream number, most sellers still have strong equity gains and can walk away with a solid profit. As Realtor.com Chief Economist Danielle Hale said, “Even after setting a more grounded price, they are likely to walk away from a sale with good money in their pocket.”

Cosmetic Fixes Aren’t a Free Pass to Overprice

One common mistake I see is sellers overestimating the value of minor upgrades. Fresh paint and light fixtures may help your home show better, but they won’t push your price $20K higher. On HGTV, when you landscape and paint, you just added $20,000 to your list, right? But that’s not the way our market is.

Updates help your home sell faster—not necessarily for more. Buyers are looking for real value, like premium locations, or renovated kitchens—not just surface-level improvements.

Price It Right from the Start—or Fall Behind

Overpricing from day one is like starting a marathon 20 miles behind everyone else. Your home lingers, buyers lose interest, and you’re forced to reduce the price later—often multiple times. At that point, your listing can go “stale,” and buyers may wonder what’s wrong with it.

Homes now spend an average of 50 days on the market—four days longer than last year, and the longest April average since 2020. As my colleague Brian Stephens of eXp Realty says, “If you overprice your home, it’s going to sit… and then you’re going to be chasing the price down.”

And it’s not just agents saying this. Even on forums like Reddit, frustrated sellers are sharing stories of regret after listing too high and getting zero offers for months.

Work With Someone Who Tells You the Truth

I always give my clients honest, data-driven pricing advice, no b.s.—even if it’s not what they hoped to hear. In fact, I’ve walked away from listings when sellers refused to adjust their expectations. A successful sale requires trust and a shared goal: to get the home sold for the best possible price in today’s market.

If you’re ready to sell, let’s talk strategy. I’ll help you price right, prepare smart, and move forward with confidence.

Thinking of Selling? Let’s Make a Plan That Works in Today’s Market

Before you list your home, make sure you’re informed, strategic, and confident. Download my free Seller’s Guide to learn what it takes to sell successfully in this market—or reach out directly and let’s discuss a pricing and marketing strategy tailored to your home and goals.

Let’s get your home sold—smart, smooth, and stress-free. — Liz Walker, RE/MAX

Thinking About Selling? These 5 Home Improvements Will Add the Most Value

If you’re a homeowner considering putting your house on the market, you’re probably wondering how to get the highest possible return. The good news? You don’t need a full renovation to make a big impact. Strategic updates—especially in key areas—can significantly increase your home’s value and appeal to potential buyers.

Here are the top 5 improvements that typically deliver the most value before selling:

1. Kitchen Refresh or Remodel

Why it matters: The kitchen is often considered the heart of the home—and buyers agree. An updated kitchen can make or break a sale.

What to do:

Repaint or refinish cabinets and countertops for a modern look.

Replace outdated hardware, faucets, and light fixtures.

Consider stainless steel appliances if yours are dated or mismatched.

ROI: A minor kitchen remodel can recoup 70–80% of its cost, and often more in hot markets.

2. Bathroom Upgrades

Why it matters: Buyers want clean, functional, and modern bathrooms. Even small improvements can make a big difference.

What to do:

Re-caulk tubs, showers, and sinks.

Replace old vanities, mirrors, and light fixtures.

Install new faucets and towel bars for a fresh, cohesive look.

Ensure plumbing and ventilation are in good working order.

Paint a dated, colored cast iron tub or sink white

ROI: Midrange bathroom updates typically recoup 60–70% of their cost.

3. Curb Appeal Enhancements

Why it matters: First impressions count. Buyers often form an opinion before they even step inside.

What to do:

Paint or replace the front door.

Clean up landscaping, trim bushes, and plant seasonal flowers.

Power-wash the exterior, walkways, and driveway.

Fix cracked concrete or damaged siding.

ROI: Basic landscaping and exterior upgrades can return 100% or more in perceived value.

4. Fresh Interior Paint

Why it matters: A fresh coat of paint is one of the most cost-effective ways to give your home a clean, updated look.

What to do:

Use neutral, light colors to appeal to the widest range of buyers.

Paint over bold or personalized colors that might turn off buyers.

Don’t forget to touch up baseboards, trim, and ceilings.

ROI: Painting can yield a 100%+ return, especially when covering outdated or damaged surfaces.

5. Flooring Updates

Why it matters: Old carpet, scratched hardwood, or outdated tile can drag down your home’s appeal.

What to do:

Replace worn carpet with midrange options or consider luxury vinyl plank (LVP), which is affordable, stylish, and durable.

Refinish hardwood floors rather than replacing them.

Fix squeaks, stains, and loose boards.

ROI: Flooring updates can deliver 70–80% ROI and drastically improve the overall feel of the home.

Bonus Tip: Declutter and Stage Smartly

Beyond physical improvements, a clean and well-staged home can help buyers envision themselves living there. Remove excess furniture, personal items, and clutter to make spaces feel larger and more inviting.

Every market is different, so it’s a smart idea to talk with a local real estate professional before making major upgrades. But generally, these five improvements offer some of the best bang for your buck. A few smart investments can lead to a quicker sale—and a higher price.

Ready to make your move? Start with a plan, prioritize these upgrades, and you’ll be well on your way to a successful sale.

As you think ahead to your own move, you may have noticed some houses sell within days, while others linger. But why is that? As Redfin says:

“. . . today’s housing market has been topsy-turvy since the pandemic. Low inventory (though rising) and high prices have created a strange mix: Some homes are flying off the market, while others sit for weeks.”

That may leave you wondering what you should expect when you sell. Let’s break it down and give you some actionable tips on how to make sure your house is one that sells quickly.

Homes Are Still Selling Faster Than Pre-Pandemic

The first thing you should know is that, in most markets, things have slowed down a little bit. While you may remember how quickly homes sold a few years ago, that’s not what you should expect today.

Now that inventory has grown, according to Realtor.com, homes are taking a bit longer to sell in today’s market (see graph below):

But before you get hung up on the ten-day difference compared to the past few years, Realtor.com will help put this into perspective:

“In April, the typical home spent 50 days on the market . . . This marks the 13th straight month of homes taking longer to sell on a year-over-year basis. Still, homes are moving more quickly than they did before the pandemic . . .”

By this comparison, if your house does take a little more time to sell this year, it’s not really a concern. It’s actually still faster than the norm. Plus, it gives you a bit more time to find your next home, which is welcome relief when you’re trying to move, too.

Just remember, some homes sell in less time than this. Some take even longer. So, what’s the real difference? Why do some homes attract eager buyers almost instantly, while others sit and struggle?

It comes down to having the right agent and strategy. Here are a few tips you need to know.

1. Price It Right

One of the biggest reasons homes sit on the market is overpricing. Many sellers want to shoot for a higher price, thinking they can lower it later – but that backfires by turning buyers away.

What to do: Work with an agent that will stick to their pricing strategy and not agree to your higher price plans. I’ll analyze recent comparable sales (what other homes have sold for recently in your area plus compare the condition of the home to yours), so you know you’re pricing appropriately for today’s market and what buyers are willing to pay. As Chen Zhao, Economic Research Lead at Redfin, explains:

“My advice to sellers is to price your home fairly for the shifting market; you may need to price lower than your initial instinct to sell quickly and avoid giving concessions.”

2. Focus on the First Impression

A messy yard or a house that needs paint? It’ll turn buyers off. Since buyers decide within seconds whether they like a home, a good first impression is key.

What to do: Outside, clean up your front yard, tidy up your landscaping, power wash walkways, and add fresh mulch. Inside, declutter and depersonalize. And consider minor touch-ups like repainting in a neutral tone. I will offer advice on what to prioritize based on your budget.

3. Strong Marketing & High-Quality Listing Photos

If your listing or your photos don’t look professional, you could have trouble drawing in buyers who think you’re trying to cut corners.

I Offer:

High-resolution, edited listing photos showing the home in its best light.

2-D Floor Plans, 3-D Interactive Floor Plan, Video Tours

Aerial Photography

Detailed descriptions that highlight SEO features of your house.

Your listing on multiple platforms, including major real estate sites

Paid and Targeted Social Media Advertising

4. The Location of the Home

You may have heard the phrase “location, location, location” when it comes to real estate. And there’s definitely some truth to that. Homes in highly sought-after neighborhoods tend to sell faster.

What to do: While you can’t change where your house is located, I can highlight the best features of your neighborhood or community in your listing. By showcasing what’s great about your area, they can help draw buyers into what life would look like in your house.

Bottom Line

Homes that sell quickly don’t necessarily have better features – they have better agents and a better strategy.

Are you thinking about selling? Let’s talk about how to get your home sold quickly and for top dollar.

Shopping for a new home is both exciting and mystifying. One of the questions you may have is how much is a down payment on a house? That can vary quite a bit, depending on the purchase price of your home, the type of loan you get, your credit score and other factors. Knowing how much down payment on a house is required can help you determine how much you need to save before looking for a home.

What is a Down Payment?

A house down payment is the portion of the home’s total purchase price that you pay upfront. Most people take out a mortgage loan to pay the balance. For example, how much is a down payment on a 300K house? If you buy a $300,000 house and you have a $30,000 down payment, you would need a $270,000 mortgage.

The down payment for a house is paid in a lump sum, at closing. The higher the down payment, the less the buyer will need to finance and the lower the monthly loan payments will be.

Is a Down Payment the Same as Earnest Money?

No, an earnest money (EM) deposit is a payment from you to the seller when you make an offer on a house. The purpose of the EM is to show the seller that you’re serious about buying the house, and it gives you time to secure financing and arrange for a home inspection. Think of it as putting a purchase on hold at a store for a small cost.

The EM is usually held in an escrow account until the deal closes and you get your keys. The EM can range from 1%–10% of the home’s price, depending on the purchase price of the property. Once the purchase is completed, the EM goes toward your down payment.

Here’s an example of how your down payment and your EM affect your mortgage amount and the amount you need to pay when your deal closes.

Purchase price

$300,000

Earnest money deposit (EM)

$3,000

Down payment for house

$30,000

Amount due at closing

$27,000 ($30,000 – $3,000)

Mortgage amount

$270,000

How Much Is a Down Payment on a House?

The amount you need for a down payment depends on the purchase price of the house, the type of loan you get to finance your purchase, your credit score, and a few other factors. These are the major loan types:

Conventional Home Loans: Typically require 3%–20% down, depending on the specific lender and your credit profile.

Federal Housing Administration (FHA) Loans: Require a minimum 3.5% down payment for borrowers with a credit score of 580 or higher. If your credit score is lower, the down payment amount is 10%.

VA Loans: Require 0% down for eligible military service members, veterans, and surviving spouses.

US Department of Agriculture (USDA) Loans: Provide 100% (0% down payment) financing for home buyers with low to average income if they’re purchasing a home in our rural WI area (as defined by the USDA).

WHEDA Loans: 100% financing available for home buyers with income and purchase limits in the State of Wisconsin.

If you’re wondering how much is the average down payment on a house, it varies based on several factors. The average down payment on a house for first-time buyers is often lower due to assistance programs, but overall, buyers typically put down between 6% and 12%.

What is Mortgage Insurance?

Mortgage insurance also known as PMI is often required by lenders (the bank, mortgage company, or person who lends you the money to pay for your house). It is a montly payment that is added on to your monthly mortage payment.

Conventional home loans usually require private mortgage insurance (PMI) if your down payment is less than 20%. This can usually be removed once you have made enough mortgage payments to cover the 20%, also known as having 20% equity in the home.

All FHA loans require mortgage insurance, which is paid directly to the FHA. This type of insurance requires an upfront fee and monthly payments, but the upfront fee can be rolled into your mortgage.

USDA and WHEDA loans also require mortgage insurance and work similarly to FHA loans, though the insurance tends to be less expensive.

For VA loans, the VA guarantees a portion of the loan, so you don’t need PMI. There is a VA funding fee due at closing, but it can be rolled into the loan amount.

Mortgage insurance is intended to protect the lender in case you don’t make your mortgage payments, or you abandon your home.

Is It Better to Make a Large Down Payment?

Yes, if you can afford it, a larger house down payment has several advantages:

Eliminates or reduces the cost of mortgage insurance

Reduces your monthly mortgage payments

Reduces the total interest paid over the life of the mortgage, which effectively lowers the cost of the house

That said, not everyone can afford a large down payment, which is why lenders and government agencies offer different options. Some home buyers also prefer to keep some cash on hand rather than applying all their savings to a down payment for a house. Although I can’t give financial advice, I can discuss your down payment with you and serve as a sounding board as you weigh your options.

How to Save for a Down Payment

Saving for a down payment can be a big challenge, especially if you’re already paying rent. However, there’s no time like the present to get started, and making a few sacrifices now will pay off when you’re able to make that down payment. Here are some tips to help you get started:

Set a savings goal: Having a specific target makes it easier to stay on track. When you see yourself making progress toward your goal, it will encourage you to keep going.

Automate savings: Set up automatic transfers to a dedicated savings account. Talk to your bank about how to set up an account that’s more difficult for you to dip into impulsively.

Reduce discretionary spending: Do an audit of your subscriptions and other periodic payments to see which ones you can eliminate. Try to cut spending on things like eating out and entertainment. This may sound impossible, but it can be done; look around the internet for tips and guides on how to save money in your everyday life.

Consider down payment assistance programs: Many states offer grants and low-interest loans to help first-time buyers.

Homebuyer Assistance Programs

There are several federal and state programs to help Americans purchase homes. Be sure to look into these, especially if your down payment for house savings is still growing.

FHA Loans: Low down payment and more lenient credit requirements.

VA Loans: No down payment is required for eligible veterans.

USDA and WHEDA Loans: No down payment for homes in our central WI qualifying rural areas.

Down Payment Plus Assistance (DPP) Programs: There are grants, forgivable loans, and tax credits available for first-time buyers. The Down Payment Plus Program offers up to $10,000 as a grant towards your down payment and closing costs.

A home inspection is a crucial safeguard for your financial future, ensuring you’re fully informed before making one of the biggest purchases of your life. An inspection can uncover major issues—like faulty wiring, hidden water damage, or structural problems—that could cost tens of thousands to repair.

Beyond financial concerns, inspections are also critical for safety. They can identify hazards like unsafe heating systems, mold, or electrical work that might cause a safety risk and not be visible during a walk-through.

A home inspection is a few hundred dollars for peace of mind. That’s far better than spending thousands later on unexpected repairs.

Should You Ever Waive a Home Inspection?

Sellers may prefer offers without an inspection contingency because it reduces the risk of last-minute renegotiations. In a competitive market, some buyers waive inspections to speed up closing and make their offers more attractive.

While I never recommend skipping an inspection, one compromise is to include an “informational-only” inspection clause in your contract. This allows you to complete an inspection but removes the expectation that the seller will make repairs.

“If major issues arise, you can still back out,” Rosalia says. “You may lose your earnest money, but that might be a small price to pay compared to the cost of unexpected repairs.”

Should You Waive an Inspection for a Recently Built Home?

Some real estate professionals argue that if a home is new or if the seller provides a recent inspection report, waiving the inspection might be a reasonable risk. However, I advise my buyers to think of it like buying a used car—you wouldn’t purchase one without having a mechanic check it first.

Many assume that new construction means fewer issues, but that’s not always the case. I had a buyer that bought a recently built home that waived the home inspection only to discover once she owned the home that the foundation settled incorrectly causing a water intrusion problem. There was also a wiring problem with the electrical panel that caused several outlets and switches not to work.

Is It Ever OK to Waive an Inspection?

Experienced investors or home flippers with construction experience and a sizable repair budget might be willing to waive an inspection, but for most buyers, it’s simply not worth the risk.

The Bottom Line

Spending a few hundred dollars on a home inspection is almost always money well spent. At the very least, it provides a useful 5yr home maintenance guide and helps buyers understand potential future repairs.

If you’re in the market for a home in Juneau County and the surrounding area I am here to help. I have several home inspectors that I’ve worked with that I can recommend to give you peace of mind when purchasing a property. With years of experience in the real estate industry, I ensure my clients make informed decisions—without unnecessary risks.

It’s surprising how often it happens, but sometimes a property just doesn’t attract buyers. Sellers may frequently ask, “Why isn’t my property selling?”. It’s important to remember that this occurs even with experienced agents and desirable homes. Fortunately, there are many potential reasons a property remains unsold, and it’s not always solely about the list price. Before resorting to a significant price drop, consider these other possible challenges and their potential solutions.

1. Suboptimal Property Characteristics

Research indicates that a substantial portion (approximately 60%) of owner-occupied residences in the United States were constructed before 1980. Certain regions have an even higher average age for homes; for instance the majority of homes built in cities like New Lisbon were built before 1970. Many of these older dwellings may lack features that are currently favored by buyers, such as generously sized bedrooms, a master bathroom, higher ceilings, multiple bathrooms, or multi-car garages. These factors can deter potential buyers from even scheduling a visit. Interestingly, sometimes newer properties built with basic materials can be more challenging to market than older homes that possess unique architectural details.

Possible Solutions:

To identify issues, I assess the property from the perspective of a modern buyer. Determine which of its attributes might be considered outdated. In some instances, sellers can address these issues through minor updates or renovations. If homeowners are unable or unwilling to modify certain problematic features, I can propose alternative strategies, such as a price reduction or offering a buyer incentive to offset the specific drawback.

2. Obvious Deficiencies in Condition

If a property appears to require significant upkeep, many prospective buyers will avoid it. Accumulating minor maintenance needs, like peeling paint, a neglected yard, or worn flooring, can be discouraging. More substantial and noticeable problems, such as unusual property layouts or outdated plumbing and electrical systems, can significantly hinder the selling process. In extreme situations, these issues can even make it difficult for buyers to secure financing.

Possible Solutions:

I would identify and clearly explain how specific deficiencies can impede a sale and offer recommendations for repairs, renovations, and property staging.

3. Inappropriate Pricing or Excessive Costs

Another frequent cause of properties not selling is simply financial: the price. Setting an excessively high price can deter potential buyers and result in a listing that remains on the market for an extended period without generating interest. Conversely, sellers and agents sometimes fail to adequately consider supplementary costs when determining the property’s price, such as homeowner association (HOA) dues, mortgage interest rates, and closing expenses. These factors influence a buyer’s affordability and, consequently, the property’s attractiveness.

Possible Solutions:

Given that most buyers carefully evaluate their potential monthly housing expenses, explore ways to adjust the price or suggest solutions to make payments more manageable. If the current interest rates are a deterrent the seller can offer a credit to the buyer to “buy down” their interest rate, meaning they will prepay interest to get a permanent rate reduction.

4. Real Estate Market Dynamics

When dealing with a property that isn’t selling, it’s essential to analyze the prevailing real estate market conditions. Various market factors can affect the sale of a home, including an oversupply of properties (a buyer’s market), economic downturns, and seasonal variations. Furthermore, local market influences can diminish the appeal of individual properties, such as the absence of convenient access to quality schools, changes in nearby businesses or industries, or even ongoing construction in the vicinity.

Possible Solutions:

Unfortunately, neither sellers nor agents can control the overall real estate market. However, gaining a deeper understanding of market trends and adopting a flexible approach is crucial. While overcoming a challenging market entirely may not be possible, you can improve the likelihood of a sale by adjusting pricing strategies, enhancing the property’s presentation, or employing creative property descriptions.

5. Inadequate Communication

Communication, though fundamental, is a significant factor in why properties fail to sell. Both the listing agent and the seller share responsibility for maintaining open and honest communication regarding the property, their expectations, concerns, and inquiries. When important details or questions are left unresolved or unaddressed, the property may be marketed ineffectively, leading to a lack of buyer interest or offers.

Possible Solutions:

Ideally, I initiate the selling process with a comprehensive presentation that sets the stage for a successful transaction so the seller knows what to expect or forsee as potential problems.

This presentation should include a market overview, staging advice, a comparative market analysis, and a clear explanation of the marketing plan.

It should also facilitate an open dialogue about the property’s condition, potential obstacles, and how to interpret feedback from marketing efforts, showings, and buyer agents.

6. Ineffective Marketing Strategies

When there are no apparent issues with the property itself or the broader real estate market, homeowners are more inclined to wonder, “Why isn’t my property generating interest?” If a property isn’t attracting sufficient attention, the marketing approach may not be as effective as it could be. It’s important to remember that even highly skilled and experienced agents can encounter this situation. Often, a minor adjustment or refinement can make a substantial difference.

Possible Solutions:

If I suspect a problem with the property’s marketing, I begin by evaluating the process as if I were a buyer’s agent searching for a similar property. If the listing appears correctly, I consider modifications to the descriptive text to boost terms used in search engines or exploring additional strategies to increase its visibility. For example, try incorporating more descriptive language into the listing description, revaluating the possible target market, or re-editing short-form videos for social media platforms

7. Poor-Quality Property Photography

Although property photography is a component of marketing, it warrants separate consideration due to its significant influence on whether a property sells. Listing photos serve as the primary point of interaction between potential buyers and the property, and inadequate photos can often cause buyers to dismiss a listing without further consideration. Photos should be high-resolution, well-lit, and captured from optimal angles. This professional presentation conveys a sense of cleanliness, freshness, and move-in readiness.

Possible Solutions:

If the seller used an agent that didn’t use a professional camera and digital editing the initial listing photos may end up subpar. Investing in a professional photographer to reshoot the property or utilizing virtual staging tools can be worthwhile . Decluttering rooms and the year to avoid including images that depict cluttered spaces, busy streets, utility lines, small or unkempt yards, or any other elements are worthwhile to improve buyers interest.

8. Property Staging and Exterior Presentation

If a property isn’t selling despite addressing the more obvious factors (price, market conditions, property quality), it may be time to concentrate on its visual appeal. Real estate data suggests that staged homes can increase the amount of money offered. While staging and landscaping don’t alter the property’s fundamental value, they can significantly enhance its attractiveness and potentially influence the final sale price.

Possible Solutions:

There are various ways to improve a property’s exterior presentation and interior staging.

Hiring a professional stager can yield the most effective results, though it can be costly.

Implementing simple staging techniques, such as decluttering and incorporating mirrors, can make a notable difference.

Similarly, basic landscaping improvements, like pruning bushes and adding container plants, can substantially enhance curb appeal.

As the peak period for residential home sales approaches, prospective buyers may encounter a broader selection of properties and increased search flexibility. This development should make it easier to buy for those who have previously struggled to locate a residence that aligns with their specific requirements.

The balance of negotiation leverage between buyers and sellers may be relatively even at present. This time last year, the market favored sellers. Currently, as the spring season commences, the market is more equal between buyers and sellers depending on the property.

It is essential to recognize that local market conditions can vary significantly, depending on what type of property you are buying. Vacation home sales are still going strong, while the local residential housing market is still a challenge for first time home buyers because there are limited properties available in the $150,000 – $250,000 price point. Here is a summary of general market trends and guidance for the upcoming months.

When does the primary period for residential real estate transactions begin?

The majority of sellers in WI typically list their properties during the spring season, starting with the spring rise in temperatures and reaching its peak in late May and early June. This timing aligns with the influx of purchasers, many of whom aim to finalize their relocation during the summer months when schools are in recess. The convergence of increased seller activity and purchaser interest characterizes spring as the most active period.

Will competitive pressures diminish in 2025?

The real estate sector is subject to seasonal fluctuations, with spring typically marking a period of heightened activity. However, fluctuations in mortgage interest rates, which have exhibited volatility over the past two years, also influence market dynamics. Decreases in interest rates tend to stimulate buyer activity, while rate increases tend to lower demand.

The average days on market for a single family home was near 3 months in the first quarter of 2025. This is double the previous year days on market of 1.5 months. It is noteworthy that competitively priced properties still tend to sell fast. I believe there has been a trend among sellers to list their property higher than the market comparisons would dictate. Sellers are still under the impression that home prices are rising quickly as happened during the Covid years but this is no longer true. The real estate market has returned to normal.

Our nation’s political climate and economy is certainly playing a large part in the movement of real estate. Buyers and sellers have been overly cautious since before the presidential election last year which has made market activity stagnant. The market isn’t crashing but it’s not quickly rising either.

Will a greater selection of affordable properties be available?

The availability of affordable properties is contingent upon individual budget constraints and local market conditions. The number of homes sold in 2024 hit a 30 year low. However, generally, experts are anticipating an increase to inventory during this spring over last year but it will be a small increase..

Will interest rate drop this year?

Consumers shouldn’t wait for interest rates to drop. The expectation is that rates will remain in the mid 6% range throughout most of the year. Economists don’t expect mortgage rates to drop below 6% this year at all. The low rates from the last five years are a thing of the past so don’t wait to make a move based on a low mortgage rate. More concerning will be the rising costs of building materials as the need for new home construction due destruction from flooding, hurricanes and wildfires. New home prices and the costs to remodel are going to continue to rise so don’t wait for the perfect time to make a move.

How much to offer on a house will depend on many factors: the current market conditions, is the property list price fair, how long it’s been on the market and your situation. Of course, every homebuyer wants to score a deal but it’s common for low ball negotiation tactics to fail.

What are the market conditions? We are currently in a very strong sellers market that means there are fewer properties for sale than buyers looking to purchase. It’s common for listings to receive multiple offers in the first week of being on the market. Sellers are expecting to get the highest price possible so offering anything less than list price will often backfire and often properties are selling over the list price. Plus, if you offer a lowball offer your could risk offending the sellers and they will write you off completely from the negotiations.

When should you offer more than the list price? This depends on your personal situation. Do you have a year or more to find the perfect home or are you in need of a home right now? Have you already had several offers get rejected and you found the perfect property? You might only get one chance at a property. Your first offer often needs to be your best offer so offering over list price is a strategy that could entice the sellers to accept your offer. Also note that in a seller’s market paying cash for a property doesn’t mean that the sellers will accept a lower price because they are expecting to receive the highest price possible.

Do seller’s come down on list price anymore? Yes, but it depends on a few things. Sellers are guided by their agent as to what the value of their home is. I can tell you from personal experience that not all sellers listen to my advice and price their property higher than it’s worth. What happens then is the home often sits on the market for a few months because buyers are doing their research and can judge for themselves whether a property is overpriced. If the property is on the market for a while then you may be successful at negotiating for a lower price. Another factor in getting a lower price is the condition or location of a property that may devalue it in the eye of the buyers.

How do you know what price to offer? This is where it pays to hire a buyer’s agent and especially one that has the experience and market knowledge to assist you. You need someone that can offer insights about market conditions, whether the property list price is accurate, is the condition of the property average or poor, what negotiation strategy to use and more. Interesting fact, 75% of real estate agents in the U.S. sold zero properties last year. Would you want to work with someone that has no experience? I wouldn’t want to trust them with the biggest purchase I’ve ever made.