If you’ve been house-hunting anywhere in Juneau County — Mauston, New Lisbon, Necedah, Elroy — you’re probably noticing the same trend buyers everywhere are talking about: rising prices, rates that won’t quit, and lenders rolling out “creative” mortgage products to keep payments lower.

One of the newest buzzwords? 50-year mortgages. Yep… lenders stretching the term way beyond the traditional 30-year just to make monthly payments more manageable.

But before you jump in, let’s break down what this actually means for you — the good, the bad, and the parts no one else is saying out loud.

🔥 The Pros of a 50-Year Mortgage

1. Lower Monthly Payments (the obvious perk)

Stretching your loan over 50 years drops your monthly payment. If you’re trying to get into a home near Castle Rock Lake, where vacation-area prices can run higher, this can be the difference between “we can swing it” and “no shot.”

2. Better Cash Flow for Your Life

Lower payments = extra bandwidth for things like:

Upgrading your place (new roof, insulation, windows — hello Wisconsin winters)

Paying down other debt

Building savings

Funding emergency repairs for septic, wells, or heating systems common in rural areas

3. Could Help First-Time Buyers Compete

When inventory is tight in towns like Mauston, Elroy, and Wonewoc, a 50-year term might make a higher-priced home achievable for buyers who are getting squeezed by interest rates.

⚠️ The Cons (you need to seriously think about these)

1. You’ll Pay Way More in Interest — Like… a lot more

A longer loan = more interest over the life of the mortgage. the total cost can be massive, like double the interest paid on a 30 year mortgage. If you already feel “rate fatigue,” a 50-year mortgage magnifies it.

2. Slower Equity Building

In Juneau County, equity matters — especially if you ever want to upgrade, buy a lake property, or sell when the market shifts. With a 50-year term, your equity grows at a snail’s pace here.

3. Risk if Property Values Don’t Keep Up

If you buy in an area where prices rise slowly (think rural outskirts between Necedah and Elroy), you could be stuck underwater longer.

4. Harder to Refinance Later

If rates drop and you want to refinance, you may not have built enough equity to make it worth it.

5. You Still Might Not Qualify

Not every lender may offer 50-year terms, and underwriting can be stricter. These products are still being discussed and not offered yet. They likely will come with higher interest rates or extra requirements.

So… Should You Consider a 50-Year Mortgage in Juneau County?

Here’s the truth: A 50-year mortgage is a tool — not a magic hack.

It works best for buyers who:

Plan to stay in the home long-term

Need the lower monthly payment to stay comfortable

Understand what they’re actually paying over time

Expect income growth in the future

Are buying a property that historically appreciates (lake homes near Castle Rock? Probably yes. Middle-of-nowhere with no upgrades? Maybe not.)

It’s not ideal for buyers who:

Want to build equity quickly

Plan to flip, upgrade, or relocate in the next 5–10 years

Are stretching too far just to “make a payment work”

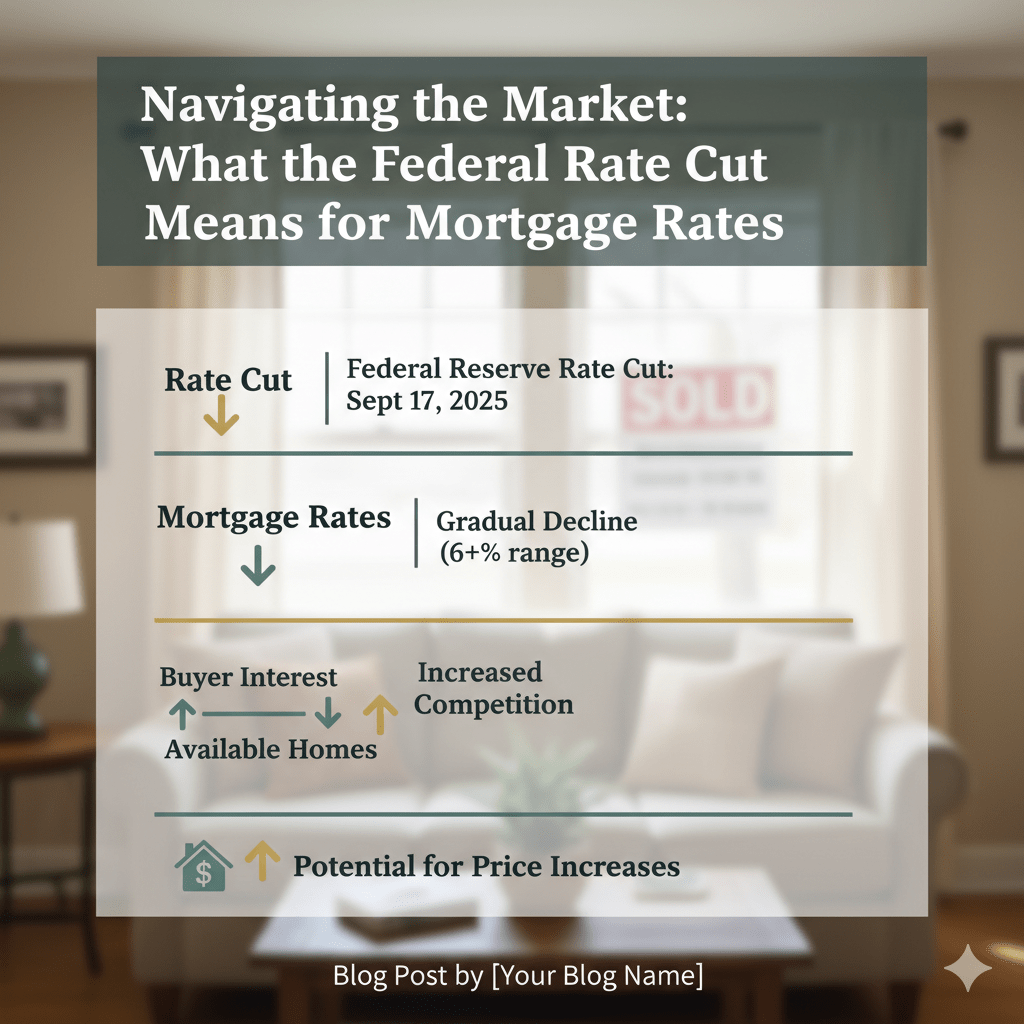

The Federal Reserve’s recent decision on September 17, 2025, to cut its benchmark interest rate by a quarter-point to a new range of 4.0% to 4.25% has homeowners and prospective buyers wondering about the impact on mortgage rates. While the news is a positive sign for borrowers, the immediate effect on mortgage rates is not as dramatic as you might think.

The Market’s Reaction: A Case of “Anticipation”

The Federal Reserve does not directly set mortgage rates. Instead, mortgage rates tend to follow the yields on long-term government bonds, such as the 10-year Treasury note. In the weeks leading up to the Fed’s announcement, the bond market had already “priced in” the widely expected rate cut. This means that investors’ anticipation of the cut had already driven mortgage rates down. For example, the average rate for a 30-year fixed mortgage had already fallen to an 11-month low of 6.35% last week.

As a result, the immediate impact of the official announcement was minimal. The White House reported that rates fell to their lowest level in three years, and Mortgage News Daily noted that the average 30-year fixed mortgage dropped 12 basis points to 6.13%. However, most of the impact was felt in the weeks leading up to the decision.

The Real Estate Market Outlook

For the housing market, this rate cut is a welcome signal. The decision was driven by concerns over a weakening labor market, which could indicate a “risk management” approach by the Fed to prevent a slowdown.

For Homebuyers: While a significant drop in mortgage rates is not expected immediately, the rate cut will likely contribute to a continued, gradual downward trend. This offers some relief and could encourage those who have been waiting on the sidelines to re-enter the market. While buyer interest will likely increase, this demand will intensify competition for available homes, which could push up prices in some areas.

For Homebuilders: The rate reduction has a direct, beneficial effect on the interest rates for construction loans. This will help reduce lending costs for builders, potentially leading to more attainable housing supply in the future.

In short, while the Fed’s rate cut is a positive development, it is not a magic bullet that will instantly slash mortgage rates. Instead, it’s a signal that provides downward pressure on rates and could help stabilize the housing market, making it a little more accessible for both homebuyers and builders. Most experts expect mortgage rates to remain above 6% through the end of the year, so if you are ready to buy, it may not be prudent to wait for a significant plunge.

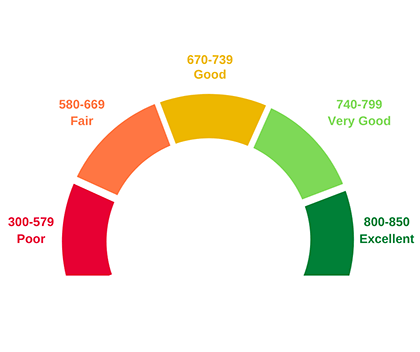

Thinking about buying your first home but worried your credit score isn’t high enough? Don’t stress—you don’t need perfect credit to become a homeowner. Many people buy homes with scores that are far from perfect. Whether your score is in the 700s or in the 500s, there are loan options that may work for you.

Why Your Credit Score Matters

Your credit score is a number that shows how well you’ve handled money in the past. Lenders use it to decide:

If you can get a loan

What interest rate you’ll pay

How much money you need to put down

A higher credit score usually means:

Better chances of getting approved

Lower interest rates (which saves you money)

Smaller down payments

Even small changes in your credit score can affect how much you pay each month. So, the higher your score, the better your deal will be.

What’s the Minimum Credit Score to Buy a Home?

Here’s a quick breakdown of the common loan types and the credit scores they usually require:

Conventional Loans

Minimum score: 620

Easier if your score is 640 or higher

Best rates if your score is 700+

If your score is on the lower end, you may pay a higher interest rate or need to show stronger proof of income.

FHA Loans

Minimum score: 500 (with 10% down)

580+ qualifies for only 3.5% down FHA loans are great for first-time buyers with lower credit scores.

VA Loans (for Veterans and Active Duty)

No official minimum score

Most lenders like to see 580–620 VA loans have no down payment and low interest rates if you qualify.

USDA Loans (for rural or small-town homes)

No set score, but most lenders want 640 or higher If your score is under 640, you’ll need more paperwork, but it’s still possible.

What If Your Credit Score Is Low?

Don’t worry—there are still ways to become a homeowner:

🏦 Check with Credit Unions or Local Banks

Some credit unions are more flexible and look at your full financial story, not just your credit score.

🏡 Way to Improve Your Credit

Apply for a credit card for a place you regularly fuel up your car like Kwik Trip, Citgo or BP. Use it only for fuel and pay it off in full every month. It takes 6 months to a year of perfect credit history but it will increase your credit score.

Pay down debt. If you have multiple credit cards or small loans, work on paying those balances down and don’t open any new accounts. Also, don’t cancel those paid off cards. Leaving them open with no balance improves your credit.

Make your payments on time.

👥 Add a Co-Signer or Co-Borrower

If a family member or partner with better credit applies with you, you may qualify for a better loan. Just remember, they’ll be responsible too if payments aren’t made.

Final Thoughts

Your credit score matters, but it’s not the only thing lenders look at. Income, savings, job history, and debt also play a big part. Even if your score isn’t great right now, there are options out there—and professionals who can help.

🏠 Ready to take the next step? Reach out to me, I can help you:

Understand your credit situation

Find loan options that match your score

Connect with lenders who are ready to work with you

You can buy a home—even with less-than-perfect credit. Let’s make your dream of homeownership a reality!

Shopping for a new home is both exciting and mystifying. One of the questions you may have is how much is a down payment on a house? That can vary quite a bit, depending on the purchase price of your home, the type of loan you get, your credit score and other factors. Knowing how much down payment on a house is required can help you determine how much you need to save before looking for a home.

What is a Down Payment?

A house down payment is the portion of the home’s total purchase price that you pay upfront. Most people take out a mortgage loan to pay the balance. For example, how much is a down payment on a 300K house? If you buy a $300,000 house and you have a $30,000 down payment, you would need a $270,000 mortgage.

The down payment for a house is paid in a lump sum, at closing. The higher the down payment, the less the buyer will need to finance and the lower the monthly loan payments will be.

Is a Down Payment the Same as Earnest Money?

No, an earnest money (EM) deposit is a payment from you to the seller when you make an offer on a house. The purpose of the EM is to show the seller that you’re serious about buying the house, and it gives you time to secure financing and arrange for a home inspection. Think of it as putting a purchase on hold at a store for a small cost.

The EM is usually held in an escrow account until the deal closes and you get your keys. The EM can range from 1%–10% of the home’s price, depending on the purchase price of the property. Once the purchase is completed, the EM goes toward your down payment.

Here’s an example of how your down payment and your EM affect your mortgage amount and the amount you need to pay when your deal closes.

Purchase price

$300,000

Earnest money deposit (EM)

$3,000

Down payment for house

$30,000

Amount due at closing

$27,000 ($30,000 – $3,000)

Mortgage amount

$270,000

How Much Is a Down Payment on a House?

The amount you need for a down payment depends on the purchase price of the house, the type of loan you get to finance your purchase, your credit score, and a few other factors. These are the major loan types:

Conventional Home Loans: Typically require 3%–20% down, depending on the specific lender and your credit profile.

Federal Housing Administration (FHA) Loans: Require a minimum 3.5% down payment for borrowers with a credit score of 580 or higher. If your credit score is lower, the down payment amount is 10%.

VA Loans: Require 0% down for eligible military service members, veterans, and surviving spouses.

US Department of Agriculture (USDA) Loans: Provide 100% (0% down payment) financing for home buyers with low to average income if they’re purchasing a home in our rural WI area (as defined by the USDA).

WHEDA Loans: 100% financing available for home buyers with income and purchase limits in the State of Wisconsin.

If you’re wondering how much is the average down payment on a house, it varies based on several factors. The average down payment on a house for first-time buyers is often lower due to assistance programs, but overall, buyers typically put down between 6% and 12%.

What is Mortgage Insurance?

Mortgage insurance also known as PMI is often required by lenders (the bank, mortgage company, or person who lends you the money to pay for your house). It is a montly payment that is added on to your monthly mortage payment.

Conventional home loans usually require private mortgage insurance (PMI) if your down payment is less than 20%. This can usually be removed once you have made enough mortgage payments to cover the 20%, also known as having 20% equity in the home.

All FHA loans require mortgage insurance, which is paid directly to the FHA. This type of insurance requires an upfront fee and monthly payments, but the upfront fee can be rolled into your mortgage.

USDA and WHEDA loans also require mortgage insurance and work similarly to FHA loans, though the insurance tends to be less expensive.

For VA loans, the VA guarantees a portion of the loan, so you don’t need PMI. There is a VA funding fee due at closing, but it can be rolled into the loan amount.

Mortgage insurance is intended to protect the lender in case you don’t make your mortgage payments, or you abandon your home.

Is It Better to Make a Large Down Payment?

Yes, if you can afford it, a larger house down payment has several advantages:

Eliminates or reduces the cost of mortgage insurance

Reduces your monthly mortgage payments

Reduces the total interest paid over the life of the mortgage, which effectively lowers the cost of the house

That said, not everyone can afford a large down payment, which is why lenders and government agencies offer different options. Some home buyers also prefer to keep some cash on hand rather than applying all their savings to a down payment for a house. Although I can’t give financial advice, I can discuss your down payment with you and serve as a sounding board as you weigh your options.

How to Save for a Down Payment

Saving for a down payment can be a big challenge, especially if you’re already paying rent. However, there’s no time like the present to get started, and making a few sacrifices now will pay off when you’re able to make that down payment. Here are some tips to help you get started:

Set a savings goal: Having a specific target makes it easier to stay on track. When you see yourself making progress toward your goal, it will encourage you to keep going.

Automate savings: Set up automatic transfers to a dedicated savings account. Talk to your bank about how to set up an account that’s more difficult for you to dip into impulsively.

Reduce discretionary spending: Do an audit of your subscriptions and other periodic payments to see which ones you can eliminate. Try to cut spending on things like eating out and entertainment. This may sound impossible, but it can be done; look around the internet for tips and guides on how to save money in your everyday life.

Consider down payment assistance programs: Many states offer grants and low-interest loans to help first-time buyers.

Homebuyer Assistance Programs

There are several federal and state programs to help Americans purchase homes. Be sure to look into these, especially if your down payment for house savings is still growing.

FHA Loans: Low down payment and more lenient credit requirements.

VA Loans: No down payment is required for eligible veterans.

USDA and WHEDA Loans: No down payment for homes in our central WI qualifying rural areas.

Down Payment Plus Assistance (DPP) Programs: There are grants, forgivable loans, and tax credits available for first-time buyers. The Down Payment Plus Program offers up to $10,000 as a grant towards your down payment and closing costs.

Why is the credit score so important? It’s the magic number lenders use to determine what type of loan you qualify for and at what interest loan. The higher the score, the lower the interest rate and the more loan options available to you. You need at least a 600 score to qualify for a government backed loan called FHA. At a 650 score you open up more options like a conventional loan. At a 750 score you coulhave a lower interest rate on a conventional loan than that 650 score.

If your score is below 600 it might be that you have no credit history! That might not make sense to you since you pay for everything on time and in cash but it’s pretty simple to increase your score. Apply for a gas card, for example from Kwik Trip. You can use it to buy your morning coffee! Keep the balance low and pay off the balance in full and on time every month. After 6 months you will have created a credit history and increased your score.

Here’s something for parents with teenagers to consider, add your kids as an authorized signer on one of your credit cards. You don’t even have to give them a card or allow them to use it. The cavaet is that your credit score passes along to them. We did this with our two kids, it enabled our son the ability to buy a car without a co-signer.

One last thing to consider, if you have a credit card you no longer use, don’t close the account. It doesn’t make sense but it will negatively affect your score. Keep the account open but cut the card up!