Thinking about building a home from the ground up? It’s an exciting journey—choosing the location, layout, finishes, and even the little details like drawer pulls in the kitchen. But one of the biggest questions I hear is: “How long is this going to take?”

The short answer: it depends. A typical home build in the U.S. takes anywhere from 6 to 12 months once construction starts. But there are a lot of moving parts, and things like weather, labor shortages, or custom features can either speed things up or slow things down.

Let’s walk through the process step by step so you know what to expect—and what could impact your timeline.

🏗️ Pre-Construction (1 to 3 Months)

Before the digging starts, there’s groundwork to cover. This includes:

Finding and buying the land

Choosing a builder or contractor

Finalizing design plans

Securing permits

Getting construction financing

This phase is often underestimated. Delays with permits, zoning, or closing on the land can set you back weeks—or even months.

🔨 Foundation (1 to 3 Weeks)

Once your lot is prepped, the crew digs and pours the foundation.

Slab foundations are quick—just a few days.

Full basements take longer due to excavation and extra structure.

Weather and soil conditions are the biggest wildcards here.

🏠 Framing & Roofing (1 to 2 Months)

This is when your house starts to look like a house! Walls go up, floors go in, the roof is framed, and windows and doors are roughed in.

Rain, snow, or cold temps can cause delays

Material shortages can also slow things down

The roof itself usually takes just a day or two to install.

⚙️ Electrical, Plumbing, & HVAC (1 to 3 Months)

This is the “behind-the-walls” work—plumbing, electrical wiring, ductwork, etc. This phase can move quickly if your contractor has a solid schedule and the trades are available. You’ll also need inspections at this stage before walls can be closed up. It’s smart to build in a buffer here just in case.

🧱 Interior & Exterior Finishes (1 to 2 Months)

Now it gets exciting again—this is where your vision comes to life:

There’s a lot happening, and coordination is key to keeping things on track.

✅ Final Walkthrough & Inspections (2 to 4 Weeks)

This last phase includes:

Touch-ups

Final inspections

Any last-minute adjustments

Once the final sign-off is done, it’s move-in time!

⏳ What Can Delay the Timeline?

Even the most well-planned projects can hit snags. Here are the common culprits:

Weather: Rain, snow, freezing temps

Permits & Inspections: Bureaucratic slowdowns or special zoning requests

Labor Shortages: Skilled trades can be booked solid

Supply Chain Issues: Delays in materials like windows or appliances

Change Orders: Changing your mind mid-build is normal—but it usually means delays and extra costs

🏡 Should You Build or Buy?

Here’s how the timelines stack up:

Buying an existing home: 1–3 months

Buying a spec home that’s under construction: 3–6 months

Building from scratch: 6–12+ months

So how long does it take to build a house? Realistically, plan for at least 6 to 12 months, knowing that custom homes may take longer. It can feel slow at times, but when it’s all said and done, you’ll have a home that’s truly yours—and that makes the wait 100% worth it.

Thinking about buying your first home but worried your credit score isn’t high enough? Don’t stress—you don’t need perfect credit to become a homeowner. Many people buy homes with scores that are far from perfect. Whether your score is in the 700s or in the 500s, there are loan options that may work for you.

Why Your Credit Score Matters

Your credit score is a number that shows how well you’ve handled money in the past. Lenders use it to decide:

If you can get a loan

What interest rate you’ll pay

How much money you need to put down

A higher credit score usually means:

Better chances of getting approved

Lower interest rates (which saves you money)

Smaller down payments

Even small changes in your credit score can affect how much you pay each month. So, the higher your score, the better your deal will be.

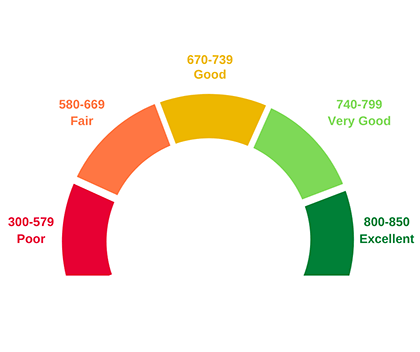

What’s the Minimum Credit Score to Buy a Home?

Here’s a quick breakdown of the common loan types and the credit scores they usually require:

Conventional Loans

Minimum score: 620

Easier if your score is 640 or higher

Best rates if your score is 700+

If your score is on the lower end, you may pay a higher interest rate or need to show stronger proof of income.

FHA Loans

Minimum score: 500 (with 10% down)

580+ qualifies for only 3.5% down FHA loans are great for first-time buyers with lower credit scores.

VA Loans (for Veterans and Active Duty)

No official minimum score

Most lenders like to see 580–620 VA loans have no down payment and low interest rates if you qualify.

USDA Loans (for rural or small-town homes)

No set score, but most lenders want 640 or higher If your score is under 640, you’ll need more paperwork, but it’s still possible.

What If Your Credit Score Is Low?

Don’t worry—there are still ways to become a homeowner:

🏦 Check with Credit Unions or Local Banks

Some credit unions are more flexible and look at your full financial story, not just your credit score.

🏡 Way to Improve Your Credit

Apply for a credit card for a place you regularly fuel up your car like Kwik Trip, Citgo or BP. Use it only for fuel and pay it off in full every month. It takes 6 months to a year of perfect credit history but it will increase your credit score.

Pay down debt. If you have multiple credit cards or small loans, work on paying those balances down and don’t open any new accounts. Also, don’t cancel those paid off cards. Leaving them open with no balance improves your credit.

Make your payments on time.

👥 Add a Co-Signer or Co-Borrower

If a family member or partner with better credit applies with you, you may qualify for a better loan. Just remember, they’ll be responsible too if payments aren’t made.

Final Thoughts

Your credit score matters, but it’s not the only thing lenders look at. Income, savings, job history, and debt also play a big part. Even if your score isn’t great right now, there are options out there—and professionals who can help.

🏠 Ready to take the next step? Reach out to me, I can help you:

Understand your credit situation

Find loan options that match your score

Connect with lenders who are ready to work with you

You can buy a home—even with less-than-perfect credit. Let’s make your dream of homeownership a reality!

Shopping for a new home is both exciting and mystifying. One of the questions you may have is how much is a down payment on a house? That can vary quite a bit, depending on the purchase price of your home, the type of loan you get, your credit score and other factors. Knowing how much down payment on a house is required can help you determine how much you need to save before looking for a home.

What is a Down Payment?

A house down payment is the portion of the home’s total purchase price that you pay upfront. Most people take out a mortgage loan to pay the balance. For example, how much is a down payment on a 300K house? If you buy a $300,000 house and you have a $30,000 down payment, you would need a $270,000 mortgage.

The down payment for a house is paid in a lump sum, at closing. The higher the down payment, the less the buyer will need to finance and the lower the monthly loan payments will be.

Is a Down Payment the Same as Earnest Money?

No, an earnest money (EM) deposit is a payment from you to the seller when you make an offer on a house. The purpose of the EM is to show the seller that you’re serious about buying the house, and it gives you time to secure financing and arrange for a home inspection. Think of it as putting a purchase on hold at a store for a small cost.

The EM is usually held in an escrow account until the deal closes and you get your keys. The EM can range from 1%–10% of the home’s price, depending on the purchase price of the property. Once the purchase is completed, the EM goes toward your down payment.

Here’s an example of how your down payment and your EM affect your mortgage amount and the amount you need to pay when your deal closes.

Purchase price

$300,000

Earnest money deposit (EM)

$3,000

Down payment for house

$30,000

Amount due at closing

$27,000 ($30,000 – $3,000)

Mortgage amount

$270,000

How Much Is a Down Payment on a House?

The amount you need for a down payment depends on the purchase price of the house, the type of loan you get to finance your purchase, your credit score, and a few other factors. These are the major loan types:

Conventional Home Loans: Typically require 3%–20% down, depending on the specific lender and your credit profile.

Federal Housing Administration (FHA) Loans: Require a minimum 3.5% down payment for borrowers with a credit score of 580 or higher. If your credit score is lower, the down payment amount is 10%.

VA Loans: Require 0% down for eligible military service members, veterans, and surviving spouses.

US Department of Agriculture (USDA) Loans: Provide 100% (0% down payment) financing for home buyers with low to average income if they’re purchasing a home in our rural WI area (as defined by the USDA).

WHEDA Loans: 100% financing available for home buyers with income and purchase limits in the State of Wisconsin.

If you’re wondering how much is the average down payment on a house, it varies based on several factors. The average down payment on a house for first-time buyers is often lower due to assistance programs, but overall, buyers typically put down between 6% and 12%.

What is Mortgage Insurance?

Mortgage insurance also known as PMI is often required by lenders (the bank, mortgage company, or person who lends you the money to pay for your house). It is a montly payment that is added on to your monthly mortage payment.

Conventional home loans usually require private mortgage insurance (PMI) if your down payment is less than 20%. This can usually be removed once you have made enough mortgage payments to cover the 20%, also known as having 20% equity in the home.

All FHA loans require mortgage insurance, which is paid directly to the FHA. This type of insurance requires an upfront fee and monthly payments, but the upfront fee can be rolled into your mortgage.

USDA and WHEDA loans also require mortgage insurance and work similarly to FHA loans, though the insurance tends to be less expensive.

For VA loans, the VA guarantees a portion of the loan, so you don’t need PMI. There is a VA funding fee due at closing, but it can be rolled into the loan amount.

Mortgage insurance is intended to protect the lender in case you don’t make your mortgage payments, or you abandon your home.

Is It Better to Make a Large Down Payment?

Yes, if you can afford it, a larger house down payment has several advantages:

Eliminates or reduces the cost of mortgage insurance

Reduces your monthly mortgage payments

Reduces the total interest paid over the life of the mortgage, which effectively lowers the cost of the house

That said, not everyone can afford a large down payment, which is why lenders and government agencies offer different options. Some home buyers also prefer to keep some cash on hand rather than applying all their savings to a down payment for a house. Although I can’t give financial advice, I can discuss your down payment with you and serve as a sounding board as you weigh your options.

How to Save for a Down Payment

Saving for a down payment can be a big challenge, especially if you’re already paying rent. However, there’s no time like the present to get started, and making a few sacrifices now will pay off when you’re able to make that down payment. Here are some tips to help you get started:

Set a savings goal: Having a specific target makes it easier to stay on track. When you see yourself making progress toward your goal, it will encourage you to keep going.

Automate savings: Set up automatic transfers to a dedicated savings account. Talk to your bank about how to set up an account that’s more difficult for you to dip into impulsively.

Reduce discretionary spending: Do an audit of your subscriptions and other periodic payments to see which ones you can eliminate. Try to cut spending on things like eating out and entertainment. This may sound impossible, but it can be done; look around the internet for tips and guides on how to save money in your everyday life.

Consider down payment assistance programs: Many states offer grants and low-interest loans to help first-time buyers.

Homebuyer Assistance Programs

There are several federal and state programs to help Americans purchase homes. Be sure to look into these, especially if your down payment for house savings is still growing.

FHA Loans: Low down payment and more lenient credit requirements.

VA Loans: No down payment is required for eligible veterans.

USDA and WHEDA Loans: No down payment for homes in our central WI qualifying rural areas.

Down Payment Plus Assistance (DPP) Programs: There are grants, forgivable loans, and tax credits available for first-time buyers. The Down Payment Plus Program offers up to $10,000 as a grant towards your down payment and closing costs.

A home inspection is a crucial safeguard for your financial future, ensuring you’re fully informed before making one of the biggest purchases of your life. An inspection can uncover major issues—like faulty wiring, hidden water damage, or structural problems—that could cost tens of thousands to repair.

Beyond financial concerns, inspections are also critical for safety. They can identify hazards like unsafe heating systems, mold, or electrical work that might cause a safety risk and not be visible during a walk-through.

A home inspection is a few hundred dollars for peace of mind. That’s far better than spending thousands later on unexpected repairs.

Should You Ever Waive a Home Inspection?

Sellers may prefer offers without an inspection contingency because it reduces the risk of last-minute renegotiations. In a competitive market, some buyers waive inspections to speed up closing and make their offers more attractive.

While I never recommend skipping an inspection, one compromise is to include an “informational-only” inspection clause in your contract. This allows you to complete an inspection but removes the expectation that the seller will make repairs.

“If major issues arise, you can still back out,” Rosalia says. “You may lose your earnest money, but that might be a small price to pay compared to the cost of unexpected repairs.”

Should You Waive an Inspection for a Recently Built Home?

Some real estate professionals argue that if a home is new or if the seller provides a recent inspection report, waiving the inspection might be a reasonable risk. However, I advise my buyers to think of it like buying a used car—you wouldn’t purchase one without having a mechanic check it first.

Many assume that new construction means fewer issues, but that’s not always the case. I had a buyer that bought a recently built home that waived the home inspection only to discover once she owned the home that the foundation settled incorrectly causing a water intrusion problem. There was also a wiring problem with the electrical panel that caused several outlets and switches not to work.

Is It Ever OK to Waive an Inspection?

Experienced investors or home flippers with construction experience and a sizable repair budget might be willing to waive an inspection, but for most buyers, it’s simply not worth the risk.

The Bottom Line

Spending a few hundred dollars on a home inspection is almost always money well spent. At the very least, it provides a useful 5yr home maintenance guide and helps buyers understand potential future repairs.

If you’re in the market for a home in Juneau County and the surrounding area I am here to help. I have several home inspectors that I’ve worked with that I can recommend to give you peace of mind when purchasing a property. With years of experience in the real estate industry, I ensure my clients make informed decisions—without unnecessary risks.

As the peak period for residential home sales approaches, prospective buyers may encounter a broader selection of properties and increased search flexibility. This development should make it easier to buy for those who have previously struggled to locate a residence that aligns with their specific requirements.

The balance of negotiation leverage between buyers and sellers may be relatively even at present. This time last year, the market favored sellers. Currently, as the spring season commences, the market is more equal between buyers and sellers depending on the property.

It is essential to recognize that local market conditions can vary significantly, depending on what type of property you are buying. Vacation home sales are still going strong, while the local residential housing market is still a challenge for first time home buyers because there are limited properties available in the $150,000 – $250,000 price point. Here is a summary of general market trends and guidance for the upcoming months.

When does the primary period for residential real estate transactions begin?

The majority of sellers in WI typically list their properties during the spring season, starting with the spring rise in temperatures and reaching its peak in late May and early June. This timing aligns with the influx of purchasers, many of whom aim to finalize their relocation during the summer months when schools are in recess. The convergence of increased seller activity and purchaser interest characterizes spring as the most active period.

Will competitive pressures diminish in 2025?

The real estate sector is subject to seasonal fluctuations, with spring typically marking a period of heightened activity. However, fluctuations in mortgage interest rates, which have exhibited volatility over the past two years, also influence market dynamics. Decreases in interest rates tend to stimulate buyer activity, while rate increases tend to lower demand.

The average days on market for a single family home was near 3 months in the first quarter of 2025. This is double the previous year days on market of 1.5 months. It is noteworthy that competitively priced properties still tend to sell fast. I believe there has been a trend among sellers to list their property higher than the market comparisons would dictate. Sellers are still under the impression that home prices are rising quickly as happened during the Covid years but this is no longer true. The real estate market has returned to normal.

Our nation’s political climate and economy is certainly playing a large part in the movement of real estate. Buyers and sellers have been overly cautious since before the presidential election last year which has made market activity stagnant. The market isn’t crashing but it’s not quickly rising either.

Will a greater selection of affordable properties be available?

The availability of affordable properties is contingent upon individual budget constraints and local market conditions. The number of homes sold in 2024 hit a 30 year low. However, generally, experts are anticipating an increase to inventory during this spring over last year but it will be a small increase..

Will interest rate drop this year?

Consumers shouldn’t wait for interest rates to drop. The expectation is that rates will remain in the mid 6% range throughout most of the year. Economists don’t expect mortgage rates to drop below 6% this year at all. The low rates from the last five years are a thing of the past so don’t wait to make a move based on a low mortgage rate. More concerning will be the rising costs of building materials as the need for new home construction due destruction from flooding, hurricanes and wildfires. New home prices and the costs to remodel are going to continue to rise so don’t wait for the perfect time to make a move.

It’s amazing what a little bit of paint can do to transform a dated kitchen! It was such an inexpensive transformation. All it took was a quart of paint and a couple of hours of labor. I’m going to pat myself on the back here because it was my suggestion. I sold the owner the home about a year ago. I stopped in this week to catch up with her and she showed me all the improvements she made. When we got to the kitchen she asked me my opinion on the cabinets as she was thinking of painting everything.

This kitchen has 1970’s style cabinets. Originally they were mostly white but with some light wood trim accents which gives it that dated look. All the appliances are black and the stone countertop has black flecks in it as well as having black cabinet hardware. So it was an easy suggestion to paint that wood trim black. The whole look changed from the dated 70’s to a modern black and white trend.

I love to chat with clients who are working through remodeling. Feel free to reach out to me if you want to bounce some ideas around on a project you are working on. I’ve been in hundreds of homes and have seen some pretty clever ideas to handle all sorts of issues. Paint tends to be the cheapest and easiest fix to dated bathroom fixtures, wood paneling, and kitchen countertops and cabinets. It certainly beats the expense of complete replacements if you don’t plan on staying in the home for a long time.

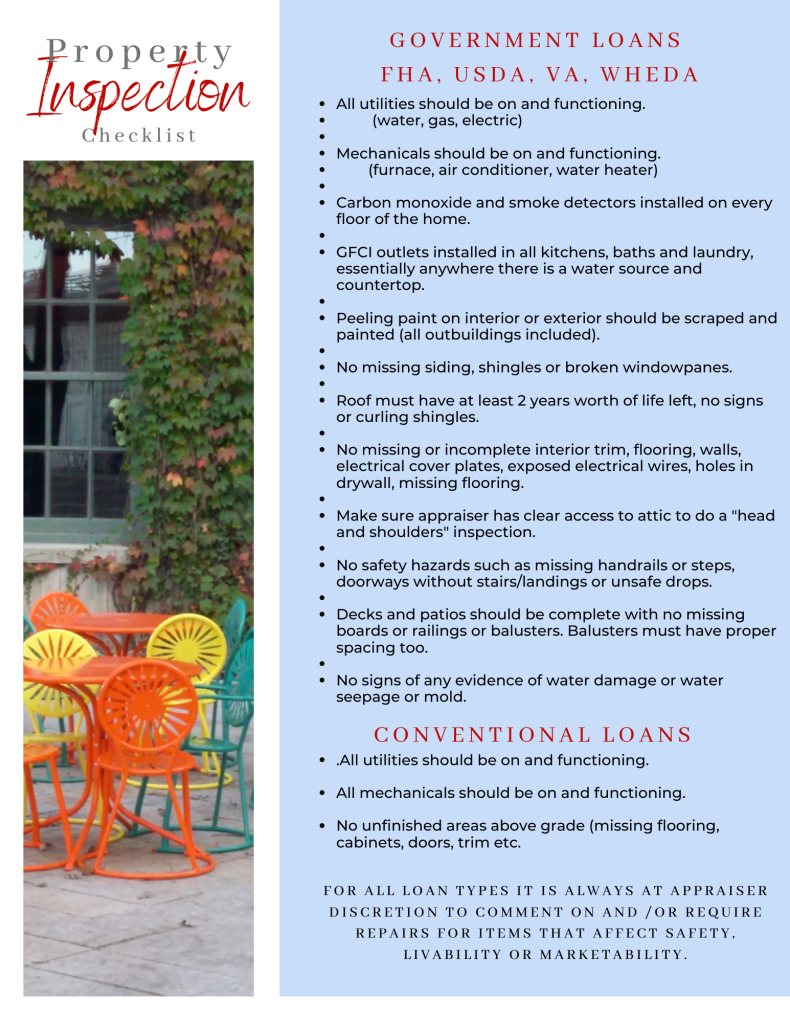

I think one of the biggest fears for sellers is a buyer that is pre-approved for a government loan program. This fear is not based on the ability of the buyer to have sufficient finances to obtain the loan but rather on the possible reasons the home could be denied for the loan. Yes, you read that right, the home can be denied.

Let me say though that with the hundreds of transactions I’ve handled, very rarely does an offer to purchase fall through due to the condition of the home. Generally, there are some basic repairs that need to be made but the seller and buyer can negotiate how to get that done. One recent case, three steps outside a home needed a handrail. I was working with the buyer and I suggested to them that they offer to build it themselves before closing. The seller was a single woman who was not in a great financial position to hire someone to get the job done. The buyer on the other hand was a couple with some basic skills so they built the handrail themselves in a matter of days.

I’ve had buyers willing to paint or scrap paint off decks. Oddly enough paint stripped off wood is fine for government loans, you just can’t have peeling paint. Other times the buyers swapped traditional outlets with GFCI outlets. For the person with the right skill set, the list of possible issues really are pretty minor things. Sellers shouldn’t fear the possiblility of repairs because a willing buyer just might do the work for you.

How much to offer on a house will depend on many factors: the current market conditions, is the property list price fair, how long it’s been on the market and your situation. Of course, every homebuyer wants to score a deal but it’s common for low ball negotiation tactics to fail.

What are the market conditions? We are currently in a very strong sellers market that means there are fewer properties for sale than buyers looking to purchase. It’s common for listings to receive multiple offers in the first week of being on the market. Sellers are expecting to get the highest price possible so offering anything less than list price will often backfire and often properties are selling over the list price. Plus, if you offer a lowball offer your could risk offending the sellers and they will write you off completely from the negotiations.

When should you offer more than the list price? This depends on your personal situation. Do you have a year or more to find the perfect home or are you in need of a home right now? Have you already had several offers get rejected and you found the perfect property? You might only get one chance at a property. Your first offer often needs to be your best offer so offering over list price is a strategy that could entice the sellers to accept your offer. Also note that in a seller’s market paying cash for a property doesn’t mean that the sellers will accept a lower price because they are expecting to receive the highest price possible.

Do seller’s come down on list price anymore? Yes, but it depends on a few things. Sellers are guided by their agent as to what the value of their home is. I can tell you from personal experience that not all sellers listen to my advice and price their property higher than it’s worth. What happens then is the home often sits on the market for a few months because buyers are doing their research and can judge for themselves whether a property is overpriced. If the property is on the market for a while then you may be successful at negotiating for a lower price. Another factor in getting a lower price is the condition or location of a property that may devalue it in the eye of the buyers.

How do you know what price to offer? This is where it pays to hire a buyer’s agent and especially one that has the experience and market knowledge to assist you. You need someone that can offer insights about market conditions, whether the property list price is accurate, is the condition of the property average or poor, what negotiation strategy to use and more. Interesting fact, 75% of real estate agents in the U.S. sold zero properties last year. Would you want to work with someone that has no experience? I wouldn’t want to trust them with the biggest purchase I’ve ever made.

Why is the credit score so important? It’s the magic number lenders use to determine what type of loan you qualify for and at what interest loan. The higher the score, the lower the interest rate and the more loan options available to you. You need at least a 600 score to qualify for a government backed loan called FHA. At a 650 score you open up more options like a conventional loan. At a 750 score you coulhave a lower interest rate on a conventional loan than that 650 score.

If your score is below 600 it might be that you have no credit history! That might not make sense to you since you pay for everything on time and in cash but it’s pretty simple to increase your score. Apply for a gas card, for example from Kwik Trip. You can use it to buy your morning coffee! Keep the balance low and pay off the balance in full and on time every month. After 6 months you will have created a credit history and increased your score.

Here’s something for parents with teenagers to consider, add your kids as an authorized signer on one of your credit cards. You don’t even have to give them a card or allow them to use it. The cavaet is that your credit score passes along to them. We did this with our two kids, it enabled our son the ability to buy a car without a co-signer.

One last thing to consider, if you have a credit card you no longer use, don’t close the account. It doesn’t make sense but it will negatively affect your score. Keep the account open but cut the card up!